Jens Bartenschlager

Jens Bartenschlager

1 min read

From M+20 to T+1: Why eSM Is the Missing Link in Accelerated Energy Settlement

This article is the second part of our eSM series exploring settlement risk in OTC energy markets. It focuses on operational readiness for faster...

This article is part of our a two-part series that provides a comprehensive analysis of the settlement risk landscape within OTC energy markets, specifically examining:

- Why settlement is the point of maximum risk in OTC energy trading

- The three distinct categories of settlement risk

- Why traditional risk mitigants are no longer sufficient

- How electronic Settlement Matching (eSM) reduces operational and timing risk.

In OTC energy trading, profit isn’t real until settlement happens.

Trades may be marked, hedged, and optimised on screen, but it’s only at settlement that notional profit & loss (P&L) turns into actual cash flow and legal title transfer. Paradoxically, this final stage is also where traders face the largest single risk exposure: the loss of the full value of delivered energy if settlement fails.

In today’s volatile market environment - shaped by renewables, broader market participation, and the aftershocks of the 2022 energy crisis, triggered by geopolitical shocks and extreme power and gas price volatility - settlement is no longer a back-office function. It has become a front-office risk concern.

Settlement Risk Is Not One Risk. It’s Three.

Settlement risk in OTC energy markets is often treated as a single concept. In reality, it consists of three distinct exposures:

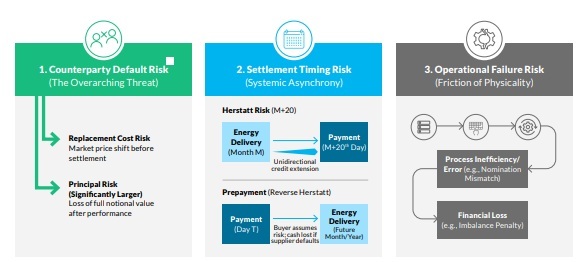

1. Counterparty Default Risk

This includes both replacement cost risk and principal risk. While replacement cost is often mitigated through variation margin, principal risk - the value of energy already delivered - is typically far larger and remains largely unsecured.

2. Settlement Timing Risk (Herstatt Risk)

Under EFET agreements, European power and gas contracts typically settle on an M+20 basis. Sellers deliver energy continuously, while buyers pay weeks later. This creates a structural, one-way credit exposure embedded directly into market design.

If a counterparty defaults between delivery and payment, the seller faces potential 100% principal loss - a modern form of Herstatt Risk, measured in weeks rather than hours.

3. Operational Failure Risk

Even when counterpartiesremain solvent, settlement can fail due to system outages, data mismatches, or manual processing errors. In tightly balanced power markets, small operational failures can translate directly into financial loss.

Why Traditional Mitigants Are No Longer Enough

Legal protections such as close-out netting, Credit Support Annexes, and central clearing remain essential pillars of risk management. However, recent market stress has shown that risk is rarely eliminated, it is redistributed.

Margining reduces counterparty exposure but increases funding and liquidity pressure. In volatile markets, otherwise solvent firms can find themselves constrained by intraday cash demands rather than credit quality.

What remains consistently under-addressed is the operational dimension of settlement risk.

electronic Settlement Matching (eSM) as a Control Layer

As settlement volumes grow and timelines compress, manual and partially automated reconciliation processes no longer scale.

eSM, based on EFET standards by Energy Traders Europe, enables automated matching of settlement data on a T+n basis. Discrepancies are identified earlier, disputes are resolved upstream, and month-end settlement risk is materially reduced.

Key benefits include:

- Earlier visibility of settlement issues

- Reduced manual intervention and operational risk

- Improved cash-flow predictability

- Greater readiness for accelerated settlement cycles

A Market in Transition

OTC energy markets are steadily moving toward shorter settlement cycles, not because of regulation, but because the capital cost of extended settlement exposure is becoming unsustainable.

Settlement is no longer where trades end. It is where risk is either realised - or controlled.

As settlement cycles accelerate and operational risk comes into sharper focus, market participants are re-evaluating how settlement data, matching, and dispute resolution are managed in practice. At Fidectus, we work with energy market participants across Europe to modernise settlement processes in line with EFET standards, underpinned by ISO-certified processes designed to meet enterprise-grade operational and security requirements.

Interested in why eSM Is the missing link in accelerated energy settlement? Then read part two of the series here.

Find out more about Settlement Hub here.

1 min read

This article is the second part of our eSM series exploring settlement risk in OTC energy markets. It focuses on operational readiness for faster...

1 min read

Settlement is the critical final stage of the trade lifecycle, where notional P&L becomes actual cash flow and physical title transfer. It is also...

1 min read

Yesterday, July 23, 2025 the White House has unveiled "Winning the Race - America's AI Action Plan". The plan is framed as a national imperative to...